Access: Make Or Break?

"Step aside Sand Hill Road, 'MANG' is now the largest VC in town!" - Apoorv Agrawal

Hello reader,

Welcome to the 50th edition of Access - our last edition was the Jobseeker Edition, featuring 102 opportunities across private capital finance, operations, and technology.

This week, we’ve been reading what industry experts are predicting for 2024. By all accounts, it’ll be a make or break year for many organisations (and their employees), with AI emerging as the dominant theme across investment trends, workplace transformation, & consumer behaviour.

It’s clear that many businesses are also operating in a cash-constrained environment, many having only just survived the turmoil of the past couple of years. If change is inevitable, how can business leaders harness tech & data to maximise revenue growth? We take a closer look.

Until next time -

Melissa & Liz

In case you missed it…

Last week, we posted our first Jobseeker Edition of 2024, with global opportunities at fund managers, technology vendors, advisors, consulting firms, and fund services providers across private markets.

FEATURING:

In Brief: The latest global private markets news, including:

VC Battlegrounds: Specialists vs. Agglomerators

Private Credit 101 🎓

Are PE Deals Finally Ready To Rebound?

In Depth: Make or Break?

IN BRIEF

Below, you’ll find a selection of global news stories from people and companies in our private markets network.

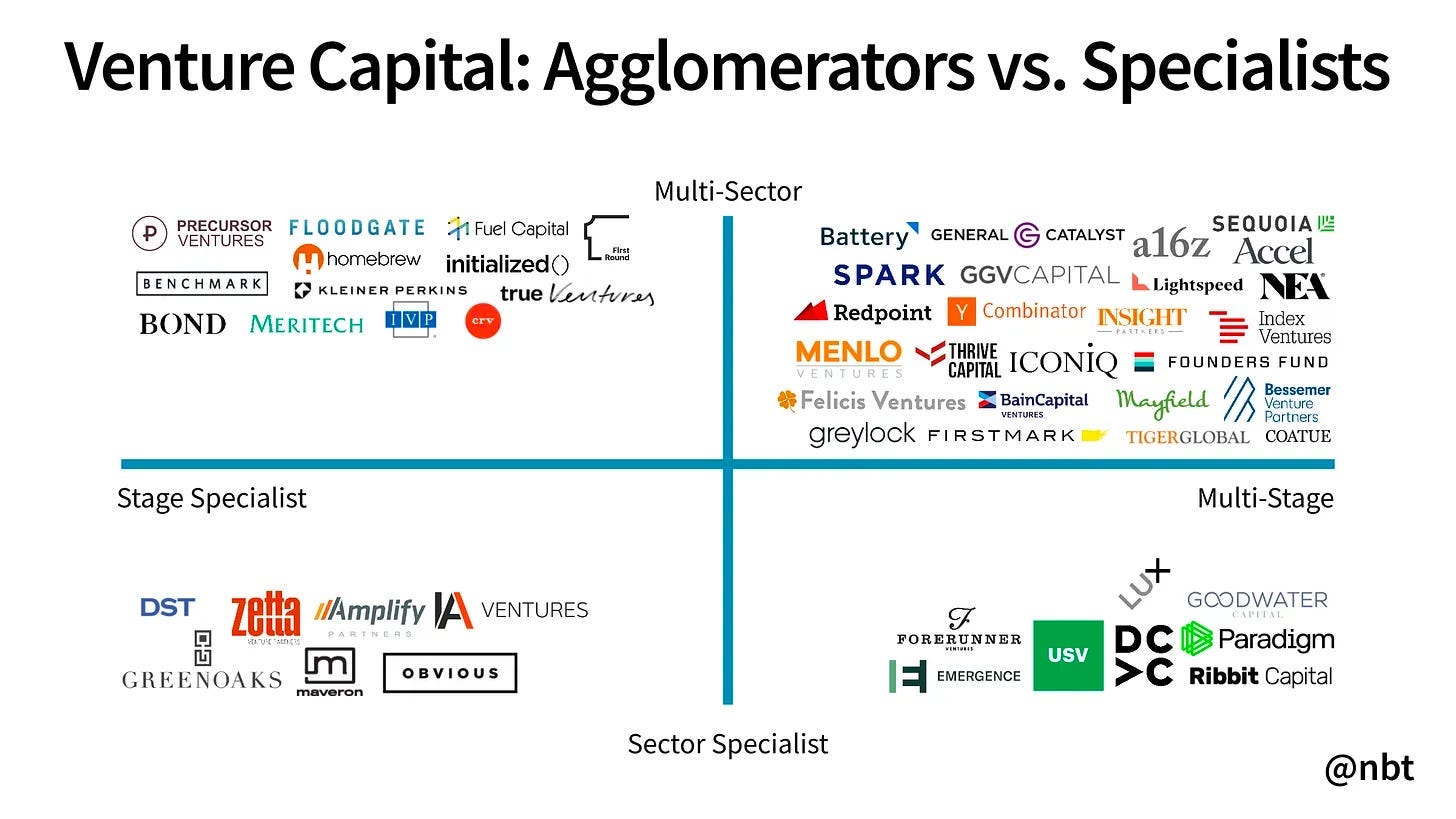

The Puritans of Venture Capital

Great piece from Kyle Harrison this week that addresses the question: “Venture used to be a cottage industry. Some firms are still practicing as if nothing really changed. Can they survive? Will capital agglomerators eat their lunch? Or can they co-exist?”

It builds on a 2020 article by Nikhil Basu Trivedi, Co-Founder & General Partner at Footwork, that outlined how the venture capital industry had bifurcated into megafunds or agglomerators (investing at every stage, across every sector) and specialists (investing by sector, stage, or both). There’s a neat matrix below that explains this:

Harrison makes a compelling argument that both types of fund need to be able to co-exist, despite the areas of conflict. For example, a potentially great company might be supported by a specialist VC early on, but needs serious amounts of cash from a so-called agglomerator to support rapid growth as it scales.

‘One of the complexities startups will face over the next few years is that a decade of excess turned the typical startup into a hungry-hungry-hippo when it comes to cash.’

- Harrison, on the downstream capital battle for VCs

***

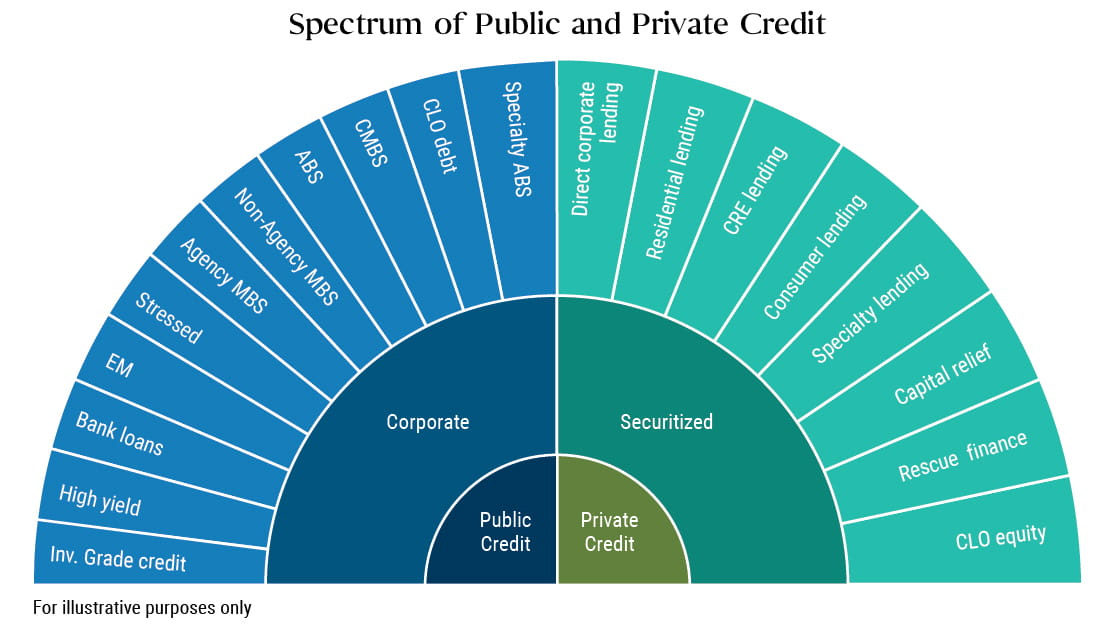

Private Credit 101 🎓

Low interest rates and regulatory changes have helped fuel the growth of private credit as an asset class, now estimated to be worth in excess of $1.5 trillion globally.

“Private equity can capture the value creation and operational improvement of private companies, while private credit can provide stable income and downside protection.”

If you’re looking for a detailed explainer on private credit, we highly recommend this piece from Anand Thaker at Private Equity Alpha. It walks through some of the history, how credit compares to PE, types of private credit, plus key risks and opportunities.

(We’ll definitely be adding it to our updated PE Essentials edition, due later this year!)

***

Are PE Deals Finally Ready To Rebound?

The FT reports that private equity executives anticipate a significant surge in takeover activities as buyout firms that have been holding on to investments in anticipation of higher prices, begin to sell off assets.

The decline in portfolio sales that the industry has seen over the past few years is expected to reverse as investors put pressure on firms to generate returns.

“For the alternatives business to work properly, there needs to be a flow of money back to [investors] for them to reinvest in the new generation of funds.”

- Anna Skoglund, Goldman Sachs

Firms with significant cash reserves are likely to see this as an opportunity to boost returns through new investments, particularly as a more pragmatic view sets in, reflecting higher financing costs and continued economic uncertainty.

“This is a good time to lean in… There is less competition for deals and multiples have come down.”

- Scott Nuttall, co-chief executive of KKR

[Read the FT’s predictions in full]

IN DEPTH

“The next big thing in 2024 will be a fresh approach to private equity predicated on data moat and business transformation with AI” - ChenLi Wang, GP at WndrCo

OnlyCFO recently declared 2024 the ‘Year of Focus & Revenue Reacceleration’. Their predictions were specifically targeted at tech firms, but could reasonably apply to many privately backed organisations. Here’s the argument in a nutshell:

Many companies have experienced a tough couple of years, with widespread layoffs, cost cutting exercises, and a constrained fundraising environment, to name just some of the challenges facing business leaders in a post-pandemic world.

While most organisations want to boost their revenue at the earliest opportunity, some are under significant pressure to do so. High revenue growth is vital if you’re planning to raise another round of funding, or for late stage companies hoping to eventually go public, for example.

Growing revenue efficiently is hard. There’s less money to throw at the problem, and more barriers to customer acquisition.

“2024 will be a year that makes or breaks a ton of companies.”

This also means that IPO readiness is likely to be a big theme for businesses and their backers, but many will use 2024 to build their track record; we may not see as many companies executing IPOs within the year.

‘[Companies] are trying to make sure they have predictability in their revenue growth, at least six quarters of strong and consistent financial performance, profitability or a very credible path to get there, and management teams and boards that are ready for being public.’ - Nikhil Basu Trivedi, GP at Footwork

AI Set To Dominate 2024

And not just 2024. Artificial Intelligence is predicted to be the 'tech theme of the decade’, with the global market expected to reach $225bn by 2027.

Not all of this will be positive - we’re already seeing significant backlash, with the New York Times suing Microsoft and OpenAI for copyright infringement. Trust is another thorny issue, in part because of the tendency for generative AI models to ‘hallucinate’, presenting incorrect information as if it were fact.

There’s also the obvious potential for disruption to existing business models, which could radically shake up entire sectors, including the possibility of job displacement. For example, decision intelligence solutions combine data science and AI to automate decision making. This can help businesses to shift gears and become more efficient (which in this environment will create much-needed competitive advantage), but as AI improves, could realistically decrease the number of human workers required.

None of this is expected to deter investors, as the sector continues its seemingly unstoppable march from science fiction to fact. Writing for the FT this week, founder of Sifted, John Thornhill reports that a ‘brassy new venture capital investor, going by the ugly acronym Mang, has been making a lot of noise in Silicon Valley.’

Mang, or Microsoft, Amazon, Nvidia and Google, have made some big bets on AI tech. While there’s nothing new about big companies investing in startups, some of these more recent investments by Mang have attracted criticism for the use of ‘credits’ in place of cash investment. There’s also the issue of whether this is a regulatory dodge to get around antitrust legislation.

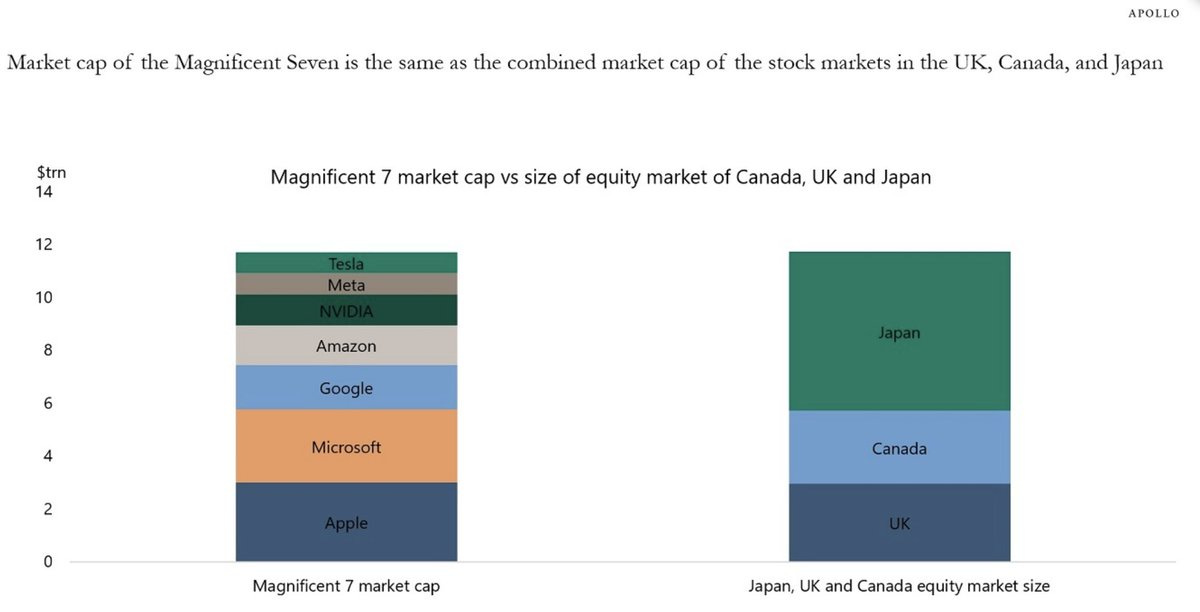

Amrita Roy notes that tech stocks have surged throughout 2023 as a result of increased interest in tools like ChatGPT, with this growth set to continue into this year. A chart published earlier this month shows how the $11.7tr market cap of the ‘Magnificent 7’ is now equal to the combined market cap of Canada, UK, and Japan.

“But how does all this affect me?”

It’s not all doom and gloom on the job front. The FT reports that ‘[Freelance talent site] Upwork found searches for “prompt engineering” began increasing from April last year, about six months after ChatGPT was released. Between the fourth quarter of 2022 and the second quarter of 2023, it recorded a 1,500 per cent increase in generative AI-related search results.’

As consumers, we can also expect to benefit from increased levels of customisation in our tech apps, combining privacy and personalisation to deliver exceptional experiences.

“Technology ultimately thrives when it meets us where we are and brings us where we want to be. Personally, I want a highly personalized agent that knows everything about me, without compromising my privacy.”

Entrepreneur Scott Belsky believes local AI models (i.e. operating on our personal devices with reduced privacy risk) will streamline daily interactions, from anticipating and making regular purchases, to handling our inboxes and calendars better than we ever did.

We can also look forward to upgraded hardware, or as Mario Gabriele describes it, 2024 is ‘The Year AI Gets a Better Body’.

“All of the miracles AI has performed in recent memory have been made from constrained hardware… It’s as if each of us has been assigned a personal genius, but we choose to consult them through a letterbox.”

Gabriele’s post is a wild read, and well worth taking the time to digest properly. A highlight for me is the description of an AI pendant from Rewind. This nifty little device is worn round your neck and records everything you say, and everything you hear, so you can replay key moments later or ask questions (e.g. what are my actions from that meeting just now?). Read in full on The Generalist, link below.

Steps to Success

Returning to OnlyCFO’s predictions for the year ahead, what can companies do to maximise revenue growth in 2024?

We’ve summarised their recommendations into two key themes: focus, and data-driven decisions.

Focus

Figure out what is the most important thing for 2024.

Thoughtfully determine what should be measured.

Get buy-in from all leaders (and other relevant employees) on all of the above. (Better yet…get them to think it’s their idea so they own it.)

Data driven decisions

Simple is usually better when it comes to metrics and other data, especially for earlier stage companies. It’s easy to get lost in data complexity.

Regularly review what you are measuring and reporting. Is it still driving the right behaviour? Is there something better we can measure?

The suggestion to determine what should be measured thoughtfully stood out for us - the article makes a great point that what gets measured, gets managed… which can either work for you or against you. It’s pivotal to select the most impactful KPIs to track, which ties in nicely with the theme of focusing on only the most important things for the year ahead.

And finally… What’s Your ‘Hit The Tennis Ball’ activity?

Peter Yang, who writes Creator Economy, reminded us of this quote from Novak Djokovic:

“I can carry on playing at this level because I like hitting the tennis ball.”

Yang asks - What’s something that you look forward to doing every day without any extrinsic rewards?

It’s got us thinking about how we want to spend the rest of our 2024. We’d love to know what your ‘tennis ball’ activities are - hit reply and let us know! We’ll pull the top responses into a post to share with you all.

Thanks for reading. If you don't want to miss our next newsletter, please add Access to your contact list. (Or move this email from "promotions" to your primary inbox.)