Access: Private Equity's Profits and Pitfalls

"You're better off paying a steep price for a great company than getting a so-so company at a bargain price." - Thomas Lee

Hello reader,

Welcome to the 40th edition of Access - our 39th edition was a profile deep dive with Nima Fara, the man selling private capital's 'hidden secret'.

Firstly - a big thank you to all of our readers who have shared Access with a friend or colleague. We really appreciate the recommendation! If you’re one of our newest subscribers, do drop us an email to say hi - you can just hit reply to the email, or leave a comment below.

Earlier this year, we wrote about ‘The Catalyst and The Capitalist’, the story of a man named Georges Doriot who many consider to be the ‘Father of Venture Capitalism’.

Doriot founded the American Research and Development Corporation (ARDC) in 1946 ‘to aid in the development of new or existing businesses into companies of stature and importance’. In its simplest form, private investment was designed to enable growth in businesses that were not considered eligible for bank loans.

Since then, private equity has acquired both champions and critics. On one side, there's the promise of potential - of breathing life into businesses, sparking innovation, and multiplying wealth. On the other, there's the shadowy reputation of stripping companies bare, the wealth of a few coming at the expense of many.

So, what makes a deal successful? The short answer is - it depends.

Whatever your perspective, one of the differentiating aspects of private equity is the element of active ownership, where fund managers roll up their sleeves and seek to influence the destiny of companies they acquire. But even in this model, there are limits to what one can control, and the vast landscape of financial markets is inherently uncertain.

This week we are taking a whistlestop tour through some of the biggest and best known private equity transactions in history to explore what known (and unknown) factors impacted the ultimate success of the deal.

Until next time -

Liz & Melissa

In case you missed it…

Last week, we shared an interview with a difference. Read the entire unedited transcript below, where Melissa Lim talks to Nima Fara about his career in financial markets and what it takes to be an exceptional sales leader.

FEATURING:

In Brief: The latest global private markets news, including:

Birkenstock Floats On NYSE

General Atlantic and Carmignac back new secondaries firm

Game on! Dynasty Equity takes a stake in Liverpool Football Club ⚽

In Depth: Private Equity's Profits and Pitfalls

IN BRIEF

Below, you’ll find a selection of global news stories from people and companies in our private markets network.

Birkenstock Floats On NYSE

Fresh from a cameo role in the recent Barbie film, German sandal maker Birkenstock has completed an initial public offering (IPO) in the US, the third-largest listing this year.

The company planned to sell at a price range of $44 to $49 per share, but Wednesday’s IPO has been described as ‘tepid’, after closing at $40.20 per share, raising yet more questions about the state of the IPO market.

The deal raised ~$1.5bn for the company and L. Catterton, Birkenstock's private equity owner - backed by luxury brand LVMH.

“Business is too good. Always. For 10 years we have been sold out.”

- Oliver Reichert, CEO at Birkenstock

Financière Agache, the family holding company of LVMH Chief Executive Bernard Arnault, the Norwegian sovereign wealth fund, and Durable Capital Partners, served as cornerstone investors.

[John Gapper thinks Birkenstock shouldn’t get too comfortable]

***

General Atlantic and Carmignac back new secondaries firm

Clipway, founded by former Ardian senior investor Vincent Gombault, has announced strategic investment from General Atlantic and Carmignac. Both firms are also reported to have committed capital to its debut fund.

The global secondaries firm employs proprietary technology and data analytics for investment opportunities. The move aligns with the trend of managers expanding into the secondaries market, driven by its growth to over $100 billion in 2022. This diversification strategy allows investors to exit illiquid private market investments early.

“Given the recent advances in technology, I believe there is a generational opportunity in bringing data science to LP secondaries investing”.

- Vincent Gombault, Managing Partner at Clipway

[You don’t have to be from Coller or Ardian to work at Clipway, but it helps]

***

Dynasty Equity takes stake in Liverpool Football Club

Continuing the trend of sports-focused investments, US private equity firm Dynasty Equity has acquired a minority stake in Liverpool Football Club.

This investment, thought to be around $100m, will be used to ensure the club's financial resilience and make infrastructure improvements at Anfield stadium. Liverpool, owned by Fenway Sports Group, had previously explored outside investment options, ultimately leading to this transaction.

Dynasty Equity was founded last year by Jonathan Nelson and K. Don Cornwell, and this marks its first investment. The duo has a history of leading and advising on sports-related deals, so it’s expected that Dynasty will make further investments in professional clubs and leagues worldwide.

“Liverpool is one of the most iconic football clubs in the world with a passionate fanbase and significant global reach. Dynasty is privileged to support the club and work alongside FSG to execute on the tremendous growth opportunities ahead.”

- K. Don Cornwell, CEO at Dynasty Equity

Read more about private equity’s blossoming relationship with the sports industry 👇

IN DEPTH

“Recognise that ultimate success comes from opportunistic, bold moves which, by definition, cannot be planned.” - Barbarians at the Gate

In this exploration of a handful of private equity deals from the past four decades, we shed light on the contrasting narratives of triumph and tribulation.

From the trailblazing RJR Nabisco deal of the 1980s to the game-changing Hilton acquisition under Blackstone's stewardship, these transactions have left indelible marks on the corporate world.

Join us as we embark on a journey through private equity's complex landscape - a terrain where potential, perception, and profits collide…

***

The One Where Private Equity Got Fracked

TXU Energy

The acquisition of TXU Energy in 2000 serves as a cautionary tale in the world of leveraged buyouts. While it was initially a headline-making deal, the subsequent financial challenges faced by the company highlight the risks associated with leveraged transactions, especially in rapidly evolving industries.

TXU, an electric and natural gas utility company based in Texas, was acquired by a consortium of PE firms, including KKR, Goldman Sachs, and Texas Pacific Group (now TPG Capital). The deal was valued at a whopping ~$45bn, a record breaker at the time. The company was renamed Energy Future Holdings.

What happened next is outlined in a fascinating post on Quora from investor Glenn Luk, that I’d absolutely recommend you read. There’s a bit of exposition about natural gas ‘well pads’, with some photos, and then Luk explains how in 1998, an engineer named Nick Steinsberger made a discovery that led to what we now call ‘hydraulic fracking’.

‘The private equity investors and bondholders had not properly factored in the potential for innovation to completely change the rules of the game.’

- Glenn Luk, investor, writing on Quora

Essentially, while the fund managers backing the deal believed that rising electricity demand would increase prices, the introduction of fracking plus industry deregulation led to energy prices tumbling. After experiencing crippling losses, the company eventually filed for bankruptcy in 2014, which was one of the largest US bankruptcies at the time.

🐍🪜🐍

The OG

RJR Nabisco

In the late 80’s, KKR made a take-private bid for RJR Nabisco, an American food & tobacco firm. It was the largest leveraged buyout at the time and remained so for many years, with a purchase price of ~$25bn that included both the acquisition of the company's outstanding shares and the assumption of its existing debt.

This colossal deal captured widespread attention and sparked a fierce bidding war, which eventually drove up the price from $75 per share to an astonishing $109 per share.

From a financial standpoint, the deal was ultimately profitable for the investors. They successfully restructured the company, sold off non-core assets, and increased its profitability. KKR eventually sold its stake in RJR Nabisco, realising significant gains.

“And I think the buyout, which I'm credited with conceiving, has certainly blossomed and is a substantial part of the financial picture of our country.”

- Jerome Kohlberg, Jr., co-founder at KKR

However, while the deal resulted in financial success for the investors, there were significant consequences for RJR Nabisco as a company. The heavy debt burden from the LBO put pressure on the company's operations, resulting in asset sales and cost-cutting measures. Additionally, the management changes and strategic shifts during the LBO period overloaded the organisation and led to long-term implications for the company's future direction.

There’s also a legacy aspect to this particular transaction, as the RJR Nabisco LBO is often cited as one of the most iconic leveraged buyouts in history. It set a precedent for large-scale LBOs and demonstrated the potential for private equity firms to generate substantial returns through financial engineering and corporate restructuring.

It was later immortalised in the bestselling book Barbarians at the Gate, increasing public awareness of high-stakes corporate takeovers and private equity-backed deals.

Iconic or notorious? You decide.

(If you’re curious about the people behind the deal, our profile of Jerome Kohlberg, cofounder at KKR, is worth a read 👇)

🐍🪜🐍

When The House Didn’t Win

Harrah’s Entertainment

The acquisition of the world’s largest casino company in 2006 was a high profile moment in the history of the gaming industry, and one of the largest deals to date in that sector. Led by Apollo Global Management, TPG Capital, and Blackstone, the transaction was valued at ~$30.7bn and represented a significant bet on the future of the gaming sector.

While the acquisition initially looked promising, the renamed Caesars Entertainment Corporation faced financial challenges and a significant debt burden in the years following the deal.

When the real estate market collapsed in the late 2000s, it had a ripple effect on the financial health of companies with high debt loads, including Caesars. At the same time, many consumers were cutting back on discretionary spending, including trips to casinos and resorts.

Ultimately, Caesars Entertainment Corporation was forced to address its financial challenges and debt issues. In 2015, the company filed for Chapter 11 bankruptcy, sparking negotiations with creditors, the separation of certain assets, and the creation of a new operating company.

After a period of transformation resulting from the bankruptcy restructuring, Caesars emerged with a new ownership structure, a reduced debt load, and a more focused approach to its operations, but the acquisition and subsequent challenges left a lasting impact on the gaming and entertainment industry.

🐍🪜🐍

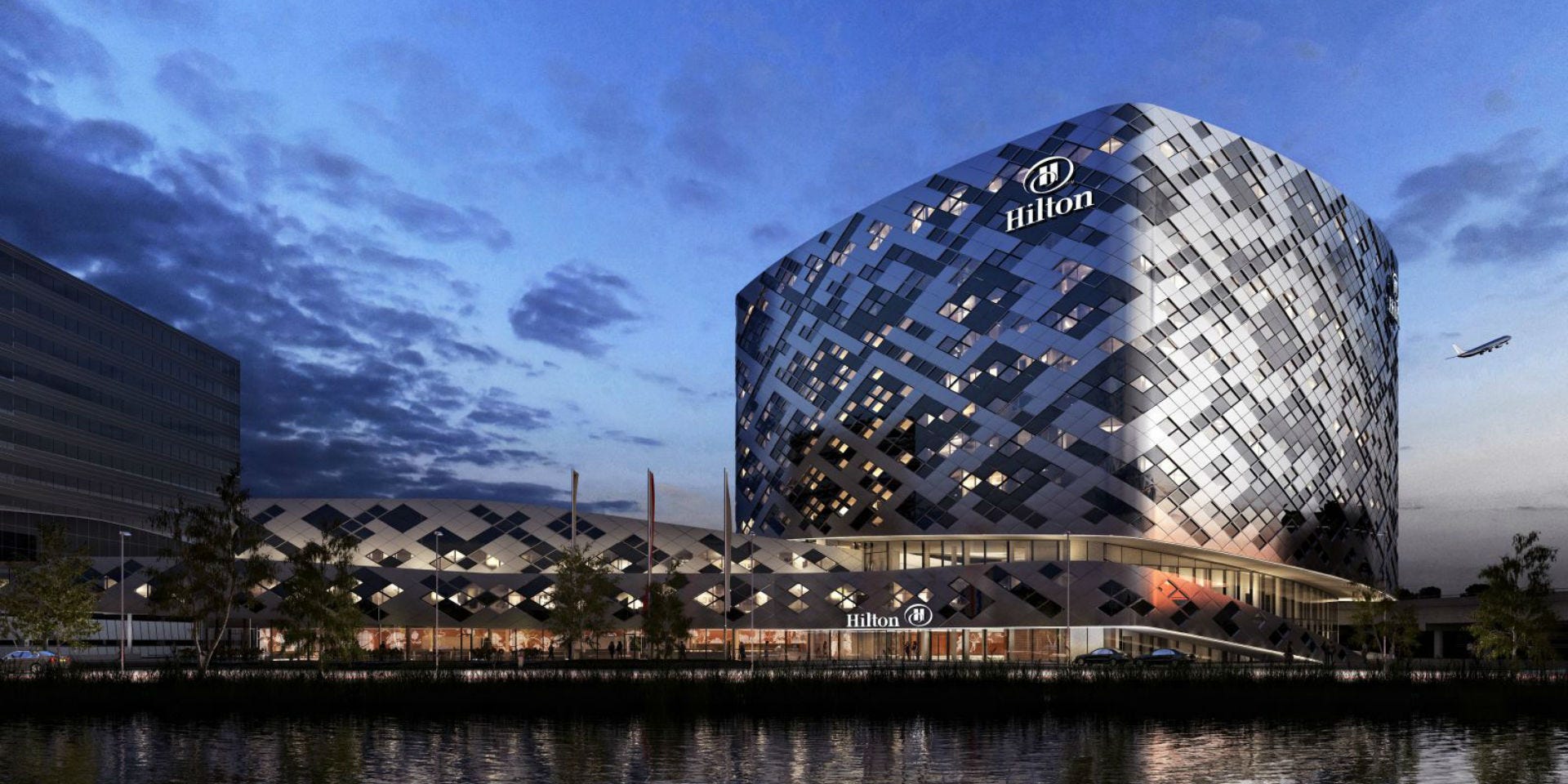

Against All Odds

Hilton Hotels

Blackstone acquired the hotel chain in 2007, at the height of the real estate bubble. With the benefit of hindsight, the timing was appalling.

The deal was valued at ~$26bn and led to the splitting of the company into three separate entities: Hilton Worldwide, Park Hotels & Resorts, and Hilton Grand Vacations. Both parties hoped the partnership would further expand Hilton's international presence and boost profitability. At the time, Hilton was already delivering substantial returns, but had accumulated significant debt while pursuing international expansion and required a partner that could facilitate global growth. Blackstone had extensive experience in the hospitality sector, and both the resources and expertise to assist, so was viewed as an ideal match.

However, in the wake of the sub-prime crisis, global revenue plummeted. Just 18-months after the purchase, the company was on the brink of collapse. So how did Hilton navigate to the successful IPO in 2013?

Under Blackstone's ownership, Hilton underwent a transformation. One of the first actions after the acquisition was the appointment of Christopher Nassetta, then Chairman of Host Hotels, as CEO.

”My father always said that “getting behind the walls” was the best way to understand a business, which is why I took my first job in the engineering department of a Holiday Inn.”

- Chris Nassetta, CEO of Hilton Hotels

During his first 100 days in role, Nassetta travelled around the world, meeting with employees working in Hilton Hotels and listening to what they had to say. It resulted in drastic action, with 90% of leadership and 80% of the head office staff being fired. Nassetta broke the news in person, describing it “as the most difficult day of my career”.

After the 2008 financial crisis hit, corporate travel declined and Hilton faced a steep uphill battle to recover its position. Nassetta is widely credited with steering Hilton through the storm by expanding the company’s global footprint and enhancing the guest experience, introducing the Hilton Honors loyalty program and digital app.

He also played a key role in returning the company to the public markets via a billion dollar IPO in 2013.

🐍🪜🐍

The Bitesized Deal

Pret A Manger

In 2018, Bridgepoint, the private equity owner of Pret A Manger, agreed to sell the UK-based sandwich shop chain to fund manager JAB Holdings for an estimated £1.5 billion. Bridgepoint had initially acquired Pret for £364m in 2008.

The deal valued Pret at approximately 15 times earnings before interest, tax, depreciation, and amortization (EBITDA), and at the time the chain operated 530 stores globally with revenues of £879 million.

Pret took a significant hit during the Covid-19 pandemic. Their initial Covid-19 response had impressed consumers; Pret rapidly moved to takeaway-only in March 2020 to protect staff and customers, while offering NHS workers free hot drinks and 50% off food orders. However, by late March Pret had shut all stores.

The company ultimately suffered crippling financial losses in the region of £250m.

Shareholders responded by investing an additional £100m into the company to support international expansion efforts, as well as opening more stores outside of London as increasing numbers of businesses shift to a hybrid working model.

“It’s been three years of transformation at Pret, in which we’ve evolved into a truly global, multichannel brand, and emerged as a stronger business than we were in 2019.”

- Pano Christou, CEO at Pret a Manger

This move to diversify outside the UK’s capital - along with the Club Pret coffee subscription service - proved successful, and in 2022 Pret reported a return to profitability for the first time since the JAB Holdings acquisition.

🐍🪜🐍

And finally… Zoo Animals Enjoy Big Pumpkins

We confess, there’s no finance link here - just some awesomely cute animals enjoying a seasonal treat. Enjoy 🎃 (and watch out for our Halloween edition coming soon!)

Thanks for reading. If you don't want to miss our next newsletter, please add Access to your contact list. (Or move this email from "promotions" to your primary inbox.)

A great read!